Iron Condor

An iron condor consists of selling an out-of-the-money bear call credit spread above the stock price and an out-of-the-money bull put credit spread below the stock price with the same expiration date.

The strategy looks to take advantage of a drop in volatility, time decay, and little or no movement from the underlying asset. Iron condors are essentially a short strangle with long option protection purchased above and below the short strikes to define risk.

Iron Condor market outlook

Iron condors are market neutral and have no directional bias. An investor would initiate an iron condor when the expectation is the stock price will stay range-bound before expiration and implied volatility will decrease.

How to set up an Iron Condor

An iron condor is created by selling a bear call credit spread and a bull put credit spread out-of-the-money with the same expiration date. The combined credit of the spreads defines the maximum profit for the trade. The maximum risk is defined by the spread width minus the credit received.

Investors can sell iron condors at any distance from the stock’s current price and with any size spread between the short and long options. The closer the strike prices are to the underlying’s price, the more credit will be collected, but the higher the probability the option will finish in-the-money.

The wider the spread width between the short and long options, the more premium will be collected, but the maximum risk will be higher.

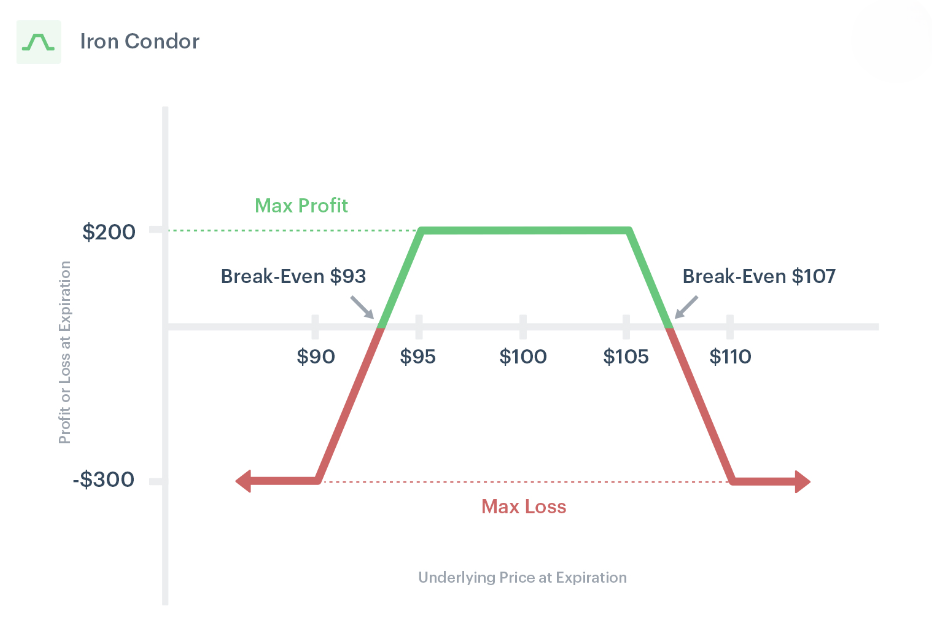

Iron Condor payoff diagram

The iron condor gets its name from the payoff diagram, which resembles a large bird’s body and wings. The profit and loss areas are well defined with an iron condor. If the price closes between the two short strike prices at expiration, the full credit is realized as a profit.

If the underlying price is above or below one of the long strike prices at expiration, the maximum loss will be realized. The break-even points are determined by the total credit received, above or below the short options.

For example, if an iron condor is opened for a $2.00 credit, the break-even price will be $2.00 above the short call strike and $2.00 below the short put strike.

Any time before expiration, there may be opportunities to close the position for a profit by exiting the full position, exiting one spread, or buying back only the short options. If the options are purchased for less money than they were sold, the strategy will be profitable.

Entering an Iron Condor

Iron condors are created by selling-to-open (STO) a credit spread above and below the current stock price. This involves selling an out-of-the-money option and buying a further out-of-the-money option.

For example, if a stock is trading at $100, a bull put spread could be opened by selling a put at the $95 strike price and buying a put at the $90 strike price. A bear call spread could be opened by selling a call at the $105 strike price and buying a call at the $110 strike price. This creates a $10 wide iron condor with $5 wide wings. If the credit received to enter the trade is $2.00, the max loss would be -$300, and the max profit potential would be $200.

- Buy-to-open: $90 put

- Sell-to-open: $95 put

- Sell-to-open: $105 call

- Buy-to-open: $110 call

The spreads can be any width and any distance from the current stock price. The closer the strike prices are to the underlying’s price, the more credit will be collected, but the higher the probability the options will finish in-the-money. The larger the width of the spread is between the short option and the long option, the more premium will be collected, but the maximum risk will be higher. The longer the expiration date is from the trade’s entry, the more premium will be collected when the position is opened, but the probability of profit will decline because there is more time for the underlying security to challenge one of the short strike prices.

Exiting an Iron Condor

Iron condors look to capitalize on time decay, minimal price movement in a stock, a drop in volatility, or a combination of all three. If the underlying stock price stays between the short options, the contracts will expire worthless, and the credit received will be kept.

Any time before expiration, there may be opportunities to close the position for a profit by exiting the full position, exiting one spread, or buying back only the short options. If the options are purchased for less money than they were sold, the strategy will be profitable.

Purchasing long option protection above and below the short strikes defines the position’s risk. The maximum loss is limited to the spread’s width minus the credit received.

If the underlying stock price is beyond the long option at expiration, the spread can be exited, and the max loss will be realized. If one of the short options is in-the-money at expiration and at risk of assignment, the contracts should be purchased if assignment is to be avoided.

Time decay impact on an Iron Condor

Time decay, or theta, works to the advantage of the iron condor strategy. Every day the time value of an options contract decreases. Ideally, the underlying stock experiences minimal movement, and theta will exponentially lose value as the position approaches expiration.

The decline in value may allow the investor to purchase the options contracts for less money than initially sold.

Implied volatility impact on an Iron Condor

Iron condors benefit from a decrease in implied volatility. Lower implied volatility results in a lower option premium. Ideally, when an iron condor is initiated, implied volatility is higher than it is at exit or expiration.

Future volatility, or vega, is uncertain and unpredictable. Still, it is good to know how volatility will affect the pricing of the options.

Adjusting an Iron Condor

Iron condors can be adjusted by extending the time horizon of the trade or by rolling one of the spreads up or down as the price of the underlying stock moves. Adjusting an iron condor typically brings in more credit, which increases the maximum profit potential, decreases the maximum risk, and widens the break-even points.

However, the position’s range of profitability decreases as the iron condor’s width tightens.

Contract size and expiration dates must remain the same to maintain the original position’s risk profile.

If one side of the iron condor is challenged as the contracts approach expiration, an investor has two choices to maximize the probability of success: roll out the position to a later expiration date or roll one of the credit spreads toward the stock price.

The entire position can be closed and reopened for a later expiration date. If this results in a credit, the break-even points will be extended by the premium received.

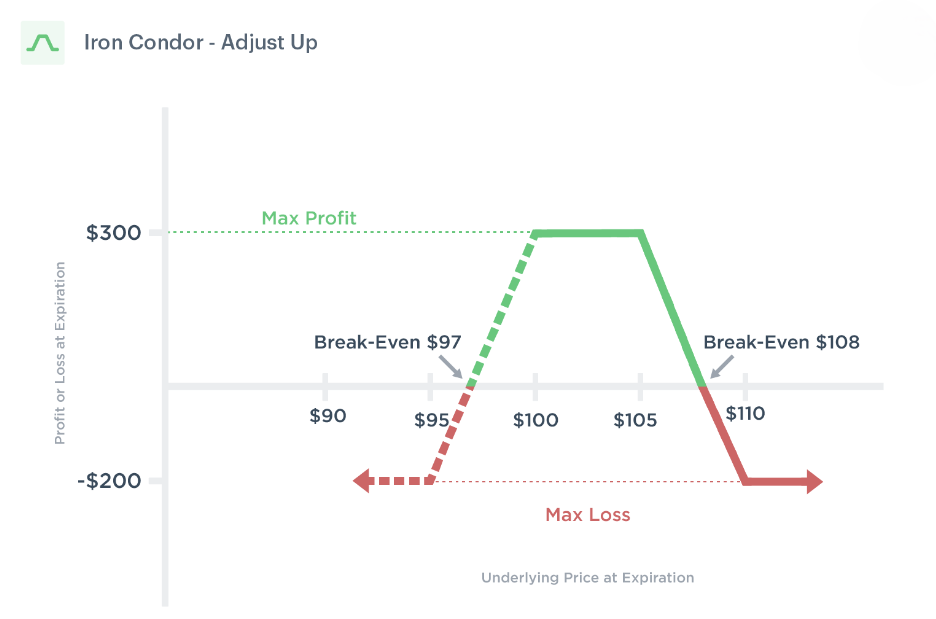

If one side of the iron condor is challenged, the opposing side could be rolled in the stock price direction to receive additional credit.

For example, if the stock is trading lower, the $105 / $110 call credit spread could be closed, and a new spread opened at a lower price. This will tighten the width of the iron condor, but the additional credit received will decrease the position’s risk.

- Buy-to-close: $105 call

- Sell-to-close: $110 call

- Sell-to-open: $100 call

- Buy-to-open: $105 call

If the adjustment brings in an additional $1.00 of credit, the maximum profit potential increases by $100 per contract, and the maximum loss decreases by $100 per contract. The break-even point for the put spread increases by the amount of credit received.

Conversely, if the stock is trading higher, the $95 / $90 put credit spread could be closed, and a new spread opened at a higher price. This will tighten the width of the iron condor, but the additional credit received will decrease the position’s risk.

- Sell-to-close: $90 put

- Buy-to-close: $95 put

- Buy-to-open: $95 put

- Sell-to-open: $100 put

If the adjustment brings in an additional $1.00 of credit, the maximum profit potential increases by $100 per contract, and the maximum loss decreases by $100 per contract. The break-even point for the call spread increases by the amount of credit received.

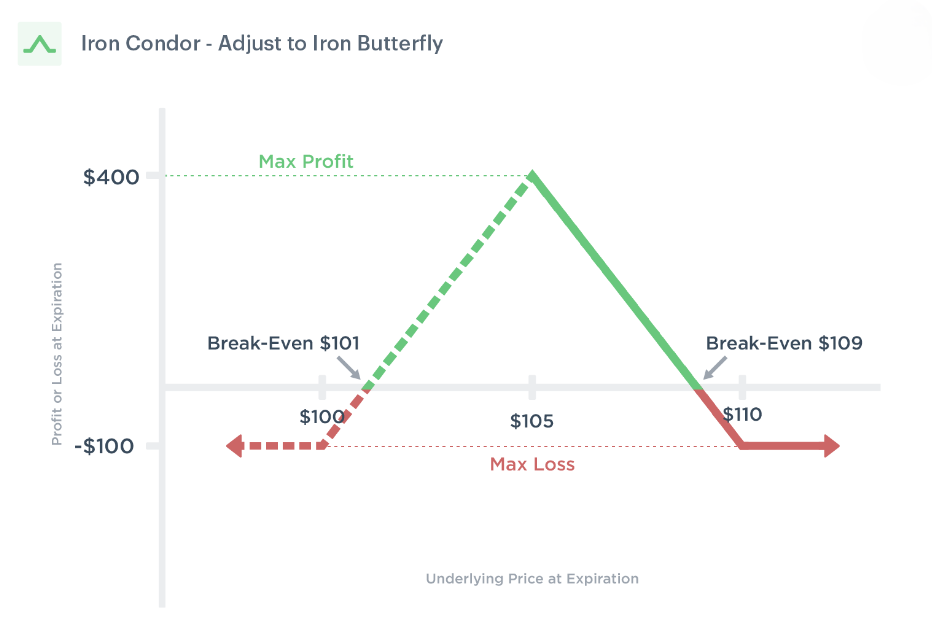

If the underlying stock’s price has moved substantially, an iron condor can be converted into an iron butterfly by closing one of the spreads and centering the short strikes at the same price.

An iron condor adjusted to an iron butterfly will have the most profit potential and least amount of risk, but the position’s range of profitability ($101 – $109) is smaller than an iron condor.

- Sell-to-close: $90 put

- Buy-to-close: $95 put

- Buy-to-open: $100 put

- Sell-to-open: $105 put

If the adjustment brings in an additional $2.00 of credit, the maximum profit potential increases by $200 per contract, and the maximum loss decreases by $200 per contract. The break-even point for the unadjusted spread will increase by the amount of credit received.

Rolling an Iron Condor

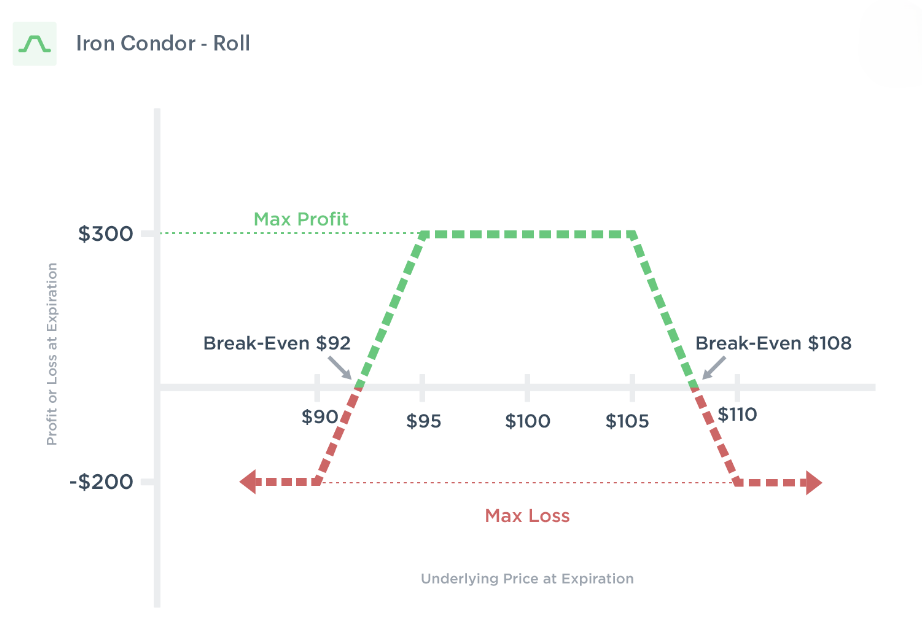

Iron condors can be rolled out to a future expiration date to maximize the trade’s potential profit. Time decay benefits options sellers. If expiration is approaching and the position is not profitable, the original iron condor position may be purchased and reopened for a future expiration date.

This may result in a credit and will extend the trade’s time duration and widen the break-even points.

For example, if the original iron condor has a $105 / $110 call spread and a $95 / $90 put spread with a June expiration date and received $2.00 of premium, an investor could buy-to-close (BTC) the entire iron condor and sell-to-open (STO) a new position in July.

If this results in a credit of $1.00, the maximum profit potential increases and the maximum loss decreases by $100 per contract. The new break-even points will be $92 and $108.

Zero Loss Adjustment (Very Important):

When the price of one leg is double of the other leg, we open a fresh short position with half the price of lower price leg at the lower price side. For example, we bought a $110 call option at $5 and $90 put option at $5 making a credit of $10. Our break-even will be at $80 and $120. If call option raises to $8 and put option falls to $4, then one option will be double than the other. At this point of time, we add another put option with price of $2 (half of $4). If even further the call option rises to $10 and combined premium of put option is $5, we sell another put option around $2.5. If even further call option prices rises and reached to $16 and combined premium of 3 put options is at $8, we exit the least premium put option and sell put option with half the premium of combined premium of 2 put options. In case price reverses we exit least premium put option when combined premium of all put options grater than or equal to call option.